Fusion funding has crossed a line you should not ignore: 17 private companies have now raised more than $100 million each, and the AI power crunch is giving investors a reason to stop treating the field as a science project.

The latest fusion funding tally is no longer just a climate story. The Next Web reported on June 20 that private investment in fusion has passed $13 billion, with 17 startups now over the $100 million mark. That is a serious signal. Money is moving into fusion because data centers are starting to make the old energy assumptions look thin.

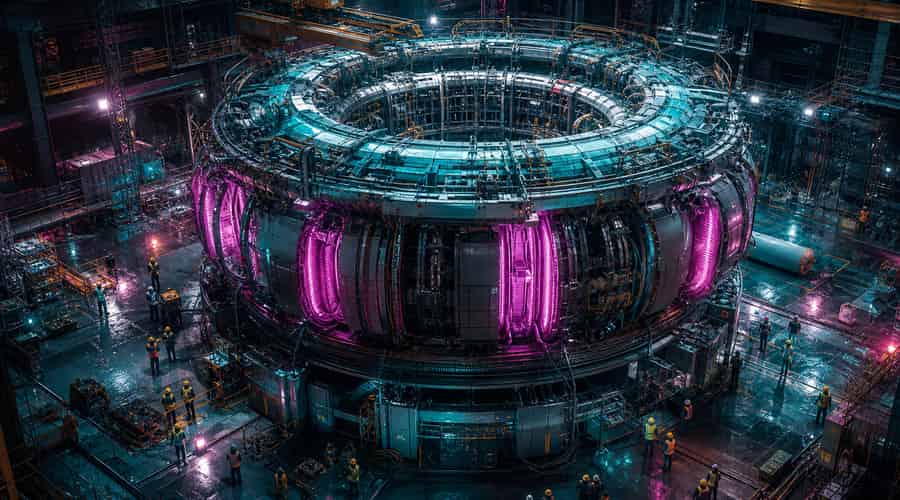

Commonwealth Fusion Systems is still the name at the front of the pack. The MIT spinout has raised roughly $3 billion, and its SPARC tokamak is being assembled at the company's campus in Devens, Massachusetts. Axios reported in January that CFS had installed the first of 18 large magnets for the machine, while announcing a digital twin project with Nvidia and Siemens at CES in Las Vegas. CFS wants SPARC to reach first plasma in 2027 and then prove a fusion gain above Q 2, with published design work pointing to a possible Q near 11. No commercial fusion reactor has done that yet. That is the point.

You do not need to believe every commercial timeline to see why investors are paying attention. CFS is not just issuing renderings. It has hardware going into a building, a planned ARC power plant in Chesterfield County, Virginia, and a 200-megawatt power purchase agreement with Google for electricity that does not exist yet. That last detail matters because the buyers are no longer theoretical utilities waiting politely at the end of the process. They are hyperscalers with a power problem now.

Helion has the same kind of customer pressure around it. The Sam Altman-backed company has raised about $1.5 billion and signed a power purchase agreement with Microsoft that targets electricity delivery in 2028. It added $425 million in a Series F round in January 2025. Pacific Fusion came out of stealth in late 2024 with a $900 million Series A. TAE Technologies has raised about $1.79 billion, and in December 2025 Trump Media agreed to merge with it in an all-stock deal valued at about $6 billion, with $200 million in cash at signing and more financing tied to regulatory filings, according to Axios and CNBC.

That TAE deal is strange, but strange does not mean irrelevant. The combined company has said it wants to begin construction in 2026 on a 50-megawatt utility-scale fusion plant and produce electricity by 2031. You should be skeptical of any fusion date that sounds too neat. Still, the financing route says something useful: fusion companies are no longer relying only on venture rounds and government programs. They are looking for public-market capital, strategic buyers, and any structure that can carry the cost of building machines measured in magnets, concrete, power electronics and years.

The honest driver is AI. Goldman Sachs has projected that hyperscaler AI infrastructure spending could reach $757 billion in 2026 and $920 billion in 2027, according to Business Insider's reporting on the bank's outlook. PCMag has also noted the brutal power difference inside the buildings themselves: AI racks can draw 60 kilowatts or more, compared with roughly 5 to 10 kilowatts for many standard data center racks. That is not a small efficiency problem. It is an electrical system problem.

Here is the thing: fusion fits the story investors want to tell about AI power better than almost anything else. It promises dense, steady, zero-carbon electricity without the intermittency of wind and solar, and without the political baggage that still follows conventional nuclear fission in many markets. Promises are cheap in fusion, and the field has spent decades proving that. But this time the demand side is different. Microsoft, Google, Nvidia, Siemens and other large technology companies are not reading fusion papers out of curiosity. They are trying to secure power before compute demand runs into the wall.

The World Economic Forum framed AI and fusion as mutually reinforcing in January, with AI tools speeding up fusion research and fusion potentially feeding the infrastructure that trained those tools. That sounds tidy, and it is a little too tidy. But CFS working with Nvidia and Siemens on a digital twin is a concrete version of the idea, not a slogan. Google DeepMind has also worked with CFS on plasma physics. The feedback loop is real enough to watch, even if it is not yet real enough to plug into the grid.

The hard part now is not whether fusion can raise attention. It has attention. The hard part is whether a 17-company field can survive the next few technical failures, delays and capital calls without collapsing into a handful of winners. Analysts at the Fusion Industry Association have expected more consolidation as better-funded companies absorb suppliers and smaller specialists. That would be normal. A sector moving from lab physics to industrial hardware always discovers that the supply chain is part of the invention.

Frankly, the $13 billion figure is impressive and clarifying at the same time. It is enough to let several approaches compete seriously: tokamaks, field-reversed configurations, inertial methods, stellarators, you name it. It is not enough to build a meaningful share of global electricity supply. If fusion is going to become infrastructure, the next pool of capital will have to be much larger, more patient, and less dazzled by clean energy mythology.

For now, the story is simpler. Fusion has moved from the edge of investor imagination into the same conversation as data centers, AI chips and grid bottlenecks. SPARC's next milestones in Devens will not settle the whole field, but they will tell you whether the private fusion boom has real engineering under it. The money has already made its bet.

Also read: Nobel laureate John Jumper leaves Google DeepMind for Anthropic as talent drains from Google's AI crown jewel • Aether AI raises $20 million to bet the next AI ceiling is causality, not compute • HyperLight's $80 million Series C is a supply-chain bet on light replacing copper in AI data centers