ASML just gave AI investors the answer they wanted: the bottleneck in advanced chips is still demand, not a missing buyer.

ASML reported €9.33 billion in second quarter sales on Wednesday, ahead of the roughly €8.8 billion analysts expected, with net income of €2.92 billion. Then it raised its full year sales outlook to between €43 billion and €45 billion, up from the €36 billion to €40 billion range it gave investors three months ago. The midpoint moved 16% higher.

You don't get that by accident.

A Monopoly Nobody Can Route Around

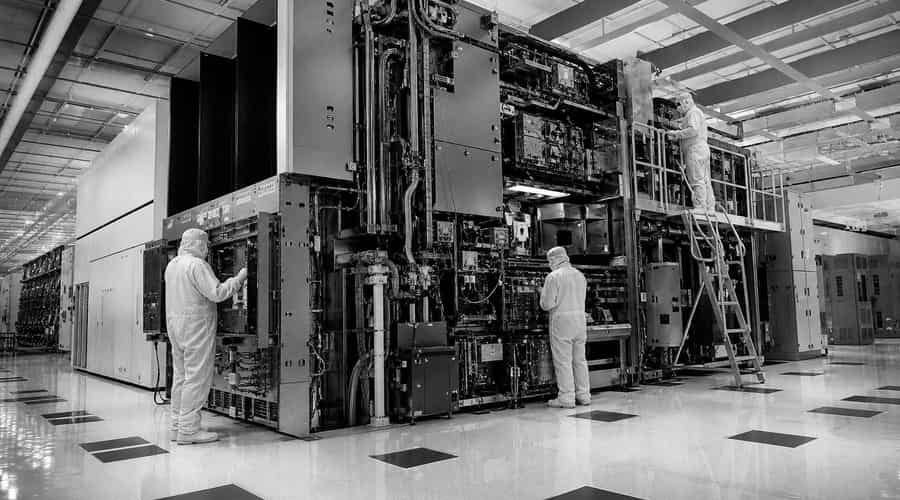

ASML is the only company in the world that makes extreme ultraviolet lithography machines, the tools chipmakers use to print the smallest circuits on advanced processors. If you want to build the kind of chip that ends up inside an Nvidia AI rack, your order eventually runs through Veldhoven, the Dutch town near Eindhoven where ASML is based. This is not a normal supplier story. It is a choke point with an earnings release.

According to the Financial Times, ASML's second quarter sales were up 21% from a year earlier, and its new full year forecast came in well above the €39.6 billion analysts had expected. The Wall Street Journal also reported that ASML lifted its expected gross margin range to 54% to 56%, from 51% to 53%. That matters for a simple reason: the terms customers accepted still left ASML with better economics, not just bigger orders.

The timing made the result sharper. IBM had just suffered its worst stock drop on record after releasing preliminary second quarter numbers on Tuesday, with revenue of $17.2 billion against the $17.86 billion analysts expected, according to MarketWatch and AP. CEO Arvind Krishna blamed part of the miss on clients shifting capital spending toward servers, storage and memory as they tried to secure supply before price increases. Software lost out to hardware.

That is not an AI demand warning. It is a spending scramble.

ASML's quarter points in the same direction. Christophe Fouquet said demand from AI infrastructure and memory customers remains strong, and the Financial Times reported that ASML is nearing full booking for 2027 EUV orders. Customers are not acting as if the cycle has rolled over. They are trying to get into the queue before the queue gets longer.

Capacity Is Now the Story

ASML now plans to raise EUV production by 30% next year and may do the same again in 2028, according to the Financial Times. That capacity gets fought over by a short list of buyers, including TSMC, Samsung and Intel, who then supply Nvidia, AMD, Apple and the cloud companies building AI data centers. If you are watching the AI trade, don't just watch Nvidia's order book. Watch the machines needed to make Nvidia's next chips.

TSMC's own numbers made the same point from the other end of the chain. Investors Business Daily reported that TSMC's June revenue rose 67.9% from a year earlier to nearly NT$443 billion, while second quarter revenue reached NT$1.27 trillion, up 36%. That was not a sleepy readout before earnings. It was another sign that the advanced node business is still running hot.

There are cracks in the story, and you should not ignore them. High NA EUV tools cost hundreds of millions of dollars, and adoption is still uneven. Intel has moved aggressively with ASML's latest systems, while TSMC has been more cautious about when the economics make sense. That is the real tension inside the rally: ASML can sell nearly everything it can build, but customers will still argue over which generation of machine is worth the bill.

China is the other risk sitting in plain sight. Investopedia noted that China accounted for about 20% of ASML's projected 2026 sales, and Dutch export controls remain tied closely to US restrictions on advanced chipmaking equipment. The newer Pax Silica framework only hardens the geopolitical backdrop. ASML can grow through that, but it can't pretend the market is politics-free.

Still, the bear case going into this week was not that AI demand was fake. It was that every chip stock already priced in years of uninterrupted growth, leaving no room for a soft quarter. ASML did not deliver a soft quarter. It raised the year, lifted margins and told investors that EUV capacity is still the limiting factor.

That is the point. If you want to know whether the AI buildout is real, look at the company whose machines have to arrive before the chips can exist. This week, ASML gave you a very plain answer.

Also read: Demis Hassabis wants a Wall Street style referee for frontier AI models, Mitsubishi Bets 7.5 Billion Dollars That Gas Power Is AI's Real Bottleneck, Dave Clark Bets His Second Act on AI Agents Running Supply Chains